Dear Investors & Partners,

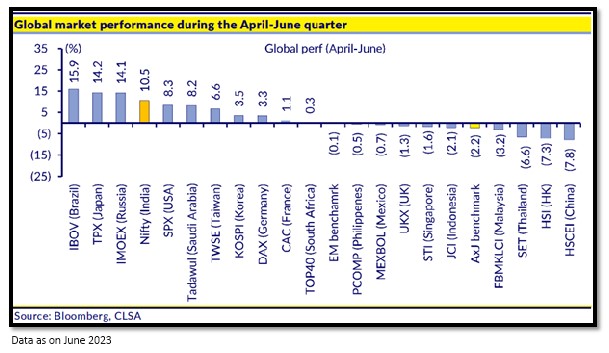

The Nifty was the fourth best performing market in the world during the April-June quarter, notably outperforming the EM (Emerging Markets) benchmark. While due to the rally in equity markets over the last 3 months, the valuations of Indian equity markets have gone up, but it is worthwhile to note that India is still expected to be the highest earnings growth market.

Markets in the month of June 2023 saw both – BSE Sensex (up 3.35% month on month) and Nifty (3.53%) scaling all-time highs. Benign inflation outlook and sustained buying momentum remained key to the stock market rally since March 2023. Strong FII support in June 2023 (Rs 47,148 crores) coupled with DII buying (Rs 4,458 crores) buoyed the markets. The above scenario clearly articulates the underlying inherent strength of the Indian economy amidst a weakening global outlook.

Key pillars of the strength of the economy:

- Strong Manufacturing PMI: Manufacturing PMI has remained above 55.0 level since July 2022, something that has not happened for a sustained period since start of the index in 2013; with new order growth at 3-month peak.

- Buoyant capex outlook: Private capex announcements grew 75% yoy to Rs. 26 lakh crore (9.6% of GDP) in FY23 vs. Rs. 15 lakh crore(6.4% % of GDP) in FY22. Notably, capex announcements by large corporates (>Rs. 3000 crore) are mostly from Green Hydrogen, Data Centers, Semiconductor, Renewables and Steel sectors. State governments' capex has also picked up in the first four months of CY23.The private sector is not holding back either, with corporate capex announcements reaching an all-time high in FY23. One area that has experienced remarkable acceleration is Data Center, as Rs. 1.4 lakh crore worth of capex has been announced for data center construction in the last two years. The Production Linked Scheme (PLI) has proven to be a game-changer for electronic goods exports (reached an all-time high)

- Services PMI holds the fort: Service PMI is reflecting even stronger trends; prospects of uptick in new activity are healthy in hospitals, airports, telecom and office space. Government spending remains strong, reflective in healthy >20% growth in construction equipment sales in FY2023 and expectation of mid-to-high teens growth for FY2024 (as per Indian Construction Equipment Manufacturers Association).

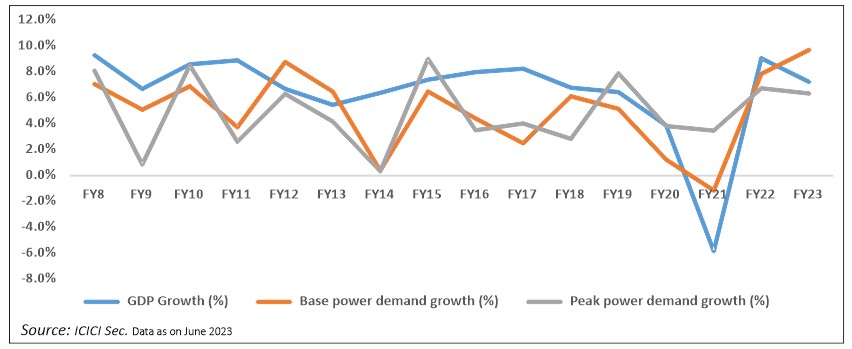

- “Power packed” New Electricity Policy: Historically, power demand in the economy has grown at a pace lower than the GDP growth. However, over the last couple of years, the power demand in the economy has grown at a multiplier of the GDP growth.

The peak power demand for the month of June touched a high of 223 GW compared to 212 GW during June 2022. Considering the sharp surge in demand, the New Electricity Policy has laid a high focus on coal as well as renewable power generation.

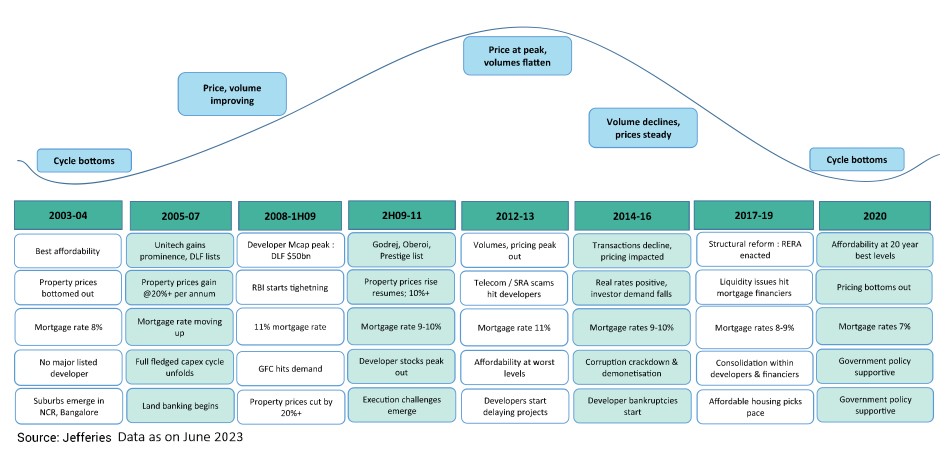

- Real Estate “upcycle” continues: As per the historical trends, the Indian Real Estate Cycle tends to move in “upcycles and downcycles” lasting over a period of 8 years each. Post 2020: Cycle has begun and we are just in the 3rd year of upcycle

- Buoyant advance tax collection figures: Tax buoyancy continues with the government’s advance tax collections for FY24 rising 15% in June quarter from a year earlier to Rs.1.15 lakh crore. The strong growth registered in advance tax collections reflects the corresponding high-frequency data such as goods and services tax (GST) collections, automobile sales and fuel consumption among others.

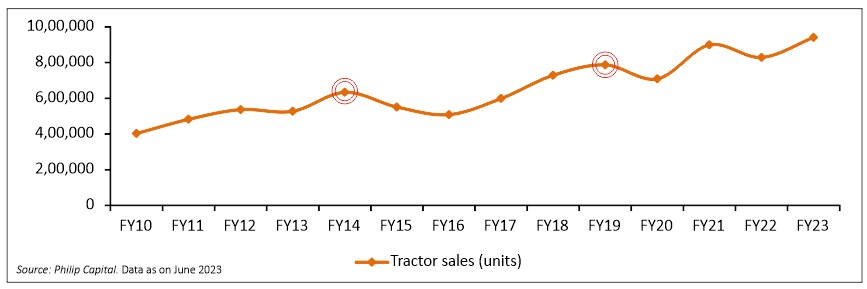

- Tractor sales tend to make new highs in the year of Loksabha Elections: Tractor unit sales over the last two Loksabha Elections (held in 2014 & 2019) point towards an interesting trend. They tend to make a “new high” in the year of Loksabha Elections. Considering the impending elections in 2024, we can expect a similar trend in this financial year as well.

While the urban consumption trends are expected to be stable, there are signs that the rural economy has bottomed out in the last quarter of FY23 after being negative for six consecutive quarters. Demand recovery is expected to sustain in this financial year with continuing moderation in inflation, healthy hike in minimum support prices for key crops and stable non-agricultural income indicators.

- FMCG Sector: Revenues of the fast-moving consumer goods (FMCG) sector are expected to grow in mid-single digits during the present financial year. It is worthwhile to note that the growth would be largely volume driven unlike price driven, a case in the past two years. Efficient companies would be able to derive significant benefits out of falling raw material prices, thereby improving upon their gross margins. A portion of the gains is expected to get ploughed back in advertising & promotional spends to ensure future revenue/market share.

For CY23, we maintain our view that India's long-term growth story is intact. India's economy should continue to exhibit strength relative to other emerging markets, based on many macro indicators including strong Govt revenue collections, low corporate and bank leverage and stable external position. This should somewhat insulate India from a global economic slowdown.

How are we positioned in our funds?

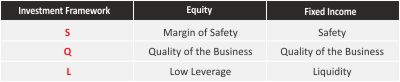

With macro situation being very dynamic and volatility increasing across asset classes, we continue with our strategy of running well-diversified portfolios. We are more focused on stock selection process within the sector rather than trying to take large overweight / underweight position among sectors. The focus continues to be on stock selection on a bottom-up basis anchored on our “SQL Investment Framework” .

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain marginally above long-term averages. On the back of lower commodity prices and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy.

Investors wanting to invest in lumpsum can invest in ITI Balanced Advantage Fund. More conservative investors can invest in the ITI Conservative Hybrid Fund, which has the potential to give better returns than traditional savings products and with much lower volatility than that of equity or aggressive hybrid funds. Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs.

Our Investment Framework – SQL

Based on our combined investment learnings of more than 50 years, we have institutionalized very strong investment Framework -SQL, which is core to our fund management framework and approach to our portfolios. We strongly believe that good quality (Q), low leverage companies (L) bought with a reasonable good margin of safety (S) makes the investment very attractive and rewarding for our investors.

Our Risk Management Framework

Our Risk Management Framework & our Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.