Dear Investors & Partners,

The domestic market recovery continued through April due to possibility of normal monsoons despite the El Nino risk, relatively benign valuations as compared to the previous years, strong domestic capex triggers driven by central and state capex and programs such as the PLI scheme. There is optimism that the rate hike cycle is close to peaking out, which will also help continue the traction in domestic economic activity level, and enable softer than earlier anticipated global slowdown. These positives have also made concerns like weak IT sector earnings and any possible fallout from US banking crises easier to swallow in the near-term.

We remain enthused by India's resilient economic performance despite global headwinds and a volatile macro environment. Three data points saw fresh peaks in April, which highlighted the underlying strength of the Indian economy, lending additional fundamental credence to our optimism.

- GST mop-up: hit a new high in April as collections rose 12% yoy to Rs1.87trn. The robust mop-up was mainly driven by a boost in year-end sales, data analytics ensuring better compliance, and sustained economic growth. The previous highest collection was Rs1.68trn in April last year, while the mop-up stood at Rs1.60trn in March this year. April 2023 also saw the highest ever tax collection on a single day as on April 20, Rs68,228cr was paid through 9.8 lakh transactions. A majority of large states reported a 20%+ yoy growth, indicating a broad-level growth across sectors and states.

- Unified Payment Interface (UPI) transactions: scaled a record high in April, clocking Rs 14.07trn in terms of value and 8.9bn in volume, rising 0.14% and 2% respectively, compared to March 2023. Compared to April 2022, transactions were higher by 59% in terms of volume and 44% in terms of value. The momentum in UPI transactions continued in April after a rise in March that was attributed to year-end transactions, especially investments, small ticket purchases and online payments.

- Daily domestic air passenger traffic also hit its all time high on last day of April as Indian carriers flew 9,593 more domestic passengers a day in April, compared to March. The average daily domestic air passenger traffic increased by 2.3% month-on-month to 428,778 passengers in April. On the other hand, the average daily international air passenger traffic in April was 1% less m-o-m at 172,058. Domestic air traffic touched an all-time high of 4,56,082 passengers in a single day on 30th April 2023. Though May traffic is likely to be impacted due to one of the major players undergoing severe disruption in engine and parts availability thereby impacting operations, the overall trajectory in a normalised environment of April indicates that the economy was well on a healthy growth path.

- Earnings season a mixed bag: In an otherwise hard time, corporate earnings were relatively healthy during 9MFY23. 4QFY23 earnings season in India started on a weak note, primarily driven by 2.5% FY24 earnings downgrade for IT services companies. The risk to earnings growth in FY24 is that the base will now have normalised, domestic slowdown in both staples and discretionary may bite, weak global growth and high interest rates may rule the roost for longer than anticipated, and US and European banking sector related volatility may impact other geographies and sectors reliant on them too.

- State capex can be a driver: FY24 state capex is likely to grow at ~22% YoY. An analysis of 19 states (comprising ~92% of state GDP) budget announced so far are indications that state fiscal deficit is likely to consolidate from 3.5% to 3.1% of GDP and there is likely to be 21.5% YoY growth in capital expenditure driven by Gujarat, AP & WB.

- Normal monsoon likely despite El Nino effect: IMD's Director has commented that El-Nino risks are moderate following the forecast of 'normal' range rainfall for the upcoming monsoon. On the positive side, reservoir levels are supportive for the next season if there were some deficiency in rainfall; reservoir levels are at 36% above LPA (Long Period Average)of ~30%. Wheat procurement this year is ongoing at a robust pace with 65% of 341 LMT (Lakh Metric Tonnes) already achieved. The current procurement of 223 LMT is already much above last year's total procurement at 188 LMT (which was severely impacted due to unseasonal rains). Other than oilseeds which is declining, other commodities are stable or rising.

- Domestic macros remain favourable: Domestic macros are favoring rural revival, barring rising risk of unseasonal rains and El Nino, the latter has historically resulted in deficient rains and lower agriculture income. Rural recovery is likely in near to medium term given a) Improvement in farm income due to rise in food grain production on a high base and higher price growth (namely wheat and rice), though the recent heat wave in the North may impact yields of wheat crop; b) Higher agriculture exports; c) Uptick in rural wages; d) Accelerated government capital spending; e) Pick-up in remittance as Covid-19 related disruptions are behind us; f) Easing inflationary pressures; g) Receding rural stress as is evident from declining MGNREGA employment; h) Resilient tractor demand; and i) Low base.

For CY23, we maintain our view that India's long-term growth story is intact. India's economy should continue to exhibit strength relative to other emerging markets, based on many macro indicators including strong Govt revenue collections, low corporate and bank leverage, and stable external position. This should somewhat insulate India from a global slowdown that sharp interest rate increases in western economies will cause.

Several factors will continue to drive India's outperformance, most of them fundamental in nature:

- External position is strong. Comfortable FX reserves (~$560bn), low external debt (around 20% of GDP and lowest amongst major economies), improving flows from remittances (World Bank estimate of 12% growth to $100bn in CY22) and abating FII selling (FII net buyers to the tune of $11bn in past four months after selling >$40bn in 9m from Oct'21) should provide support to the rupee.

- While the US and EU combat inflation, India has not suffered as severely; policy rates are up by much less than in the West.

- PMI both Services and Mfg. above 55 for many months.

- Tax collections above 15% for Centre and 25% for states.

- Corporate leverage down by 10ppt (percentage point) in last eight years to 31% of GDP.

- Capex momentum is picking up and the policy environment is supportive. However, a full-blown capex recovery is likely only in 2024.

- Overall policy environment is supportive with focus on structural economic reforms like financial inclusion, DBT, Make-in-India, GST, RERA, Bankruptcy court beginning to yield results.

- Banks are in better health after getting past NPA and NBFC crisis of 2015-2018 period. NPAs have come off from the peak of 11.2% in FY18 to 5.9% in FY22. Even after recent concerns raised over the debt exposure to a large corporate group highlighted by a set of investors, disclosures indicated that bank loans to the group have been largely stable over FY2019-22, and well below their prescribed exposure limits. This once again reinstates the view that banking sector health is much better as compared to in the past and there appears to be less probability of a large risk to asset quality of banks, which have seen consistent improvement in recent years.

- India's CAD will likely expand over 3.5% of GDP due to high commodity prices, but if crude stays near current levels of US$85/bbl, CAD can dip below 3%, and the rupee can stay stable.

How are we positioned in our funds?

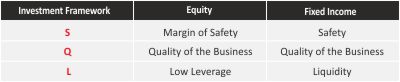

With macro situation being very dynamic and volatilities across asset classes increasing, we continue with our strategy of running well diversified portfolios. We are more focused on stock selections within the sector rather than trying to take large overweight / underweight positions among sectors. The focus continues to be on stock selection on a bottom-up basis anchored on our “SQL Investment Framework”

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain slightly above long-term averages. We have observed in the past that whenever crude has corrected due to demand destruction in economic recessions, India's earnings growth and market performance have not remained immune. However, if crude prices correct due to increase in supplies, India will definitely benefit. Coupled with lower prices of other commodities too, and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy.

Investors wanting to invest in lumpsum can invest in ITI Balanced Advantage Fund. More conservative investors can invest in the ITI Conservative Hybrid Fund, which has the potential to give better returns than traditional savings products and with much lower volatility than that of equity or aggressive hybrid funds. Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs.

Our Investment Framework – SQL

Based on our combined investment learnings of more than 50 years, we have institutionalized very strong investment Framework -SQL, which is core to our fund management framework and approach to our portfolios. We strongly believe that good quality (Q), low leverage companies (L) bought with a reasonable good margin of safety (S) makes the investment very attractive and rewarding for our investors.

Our Risk Management Framework

Our Risk Management Framework & our Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.