Dear Investors & Partners,

Equity Update

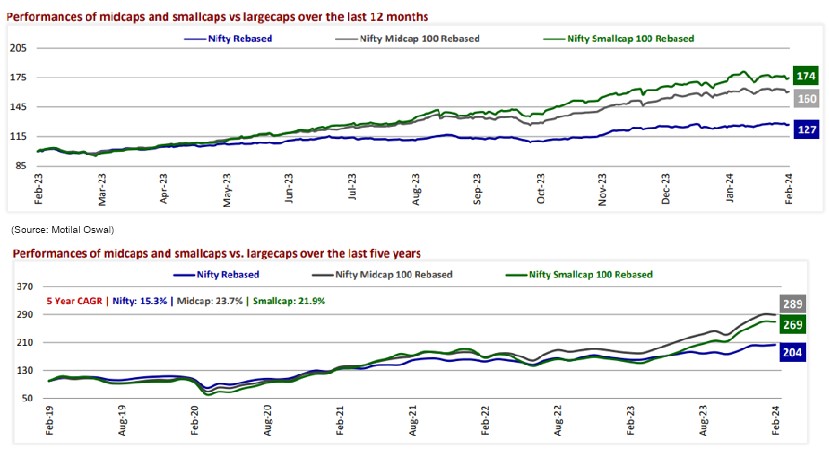

The month of February 2024 continued to be volatile as was seen in January as well, though the Nifty managed to close up by 1.2% MoM. This was even after the spectacular rally in the markets over the past 12 months, when midcaps 150 and small caps 250 have gained 60% and 74%, respectively, while large caps 100 have risen 27%.

(Source: Motilal Oswal)

Past performance may or may not be sustained in future and is not a guarantee of any future returns. Index performance does not signify scheme performance.

Mixed earnings season: The corporate earnings season was mixed in general, as domestic cyclicals such as Autos and Financials, along with global cyclicals like Metals and Oil & Gas performed well vis-à-vis expectations. On the other hand, Technology posted a marginal decline in earnings, its first in 26 quarters. Moreover, the number of companies delivering positive earnings surprise in 3QFY24 was lowest since Mar-20, indicating a higher level of expectations on corporate sales and profitability growth.

DII flows sustain: In Feb'24, FIIs posted the muted inflows at USD 0.5bn. DIIs recorded the seventh consecutive month of inflows at USD 3.1bn. FII outflows into Indian equities stood at USD 2.7b in YTD CY24 vs inflows of USD 21.4b in CY23. DII inflows into equities in YTD CY24 continue to be strong at USD 6.3b vs USD 22.3b in CY23.

Sector breadth balanced: Among the sectors, PSU Banks (+10%), Real Estate (+6%), Automobiles (+6%), Healthcare (+6%), and Oil & Gas (+6%) were the top gainers. On the other hand, Media (-5%), Private Banks (-2%), Consumer (-2%), and Metals (-1%) were the key laggards.

Healthy GDP growth: Real GDP growth crossed 8% for the third successive quarter in 3QFY24 vs 8.1% (revised higher from 7.6%) in 2QFY24 and 4.3% in 3QFY23 (revised lower from 4.8%). 1QFY24 GDP growth was also revised higher to 8.2% from 7.8%. Consequently, GDP growth for 9MFY24 stood at 8.2%. Higher-than-expected GDP growth was partly led by a downward revision in 3QFY23 growth (to 4.3% from 4.8% earlier) and a very high growth in real net indirect taxes, driven by lower subsidies.

Private investment cycle recovery will be key: While there was a sharp increase in corporate profitability since FY20, private capex pickup had relatively lagged. Capex increased 26% in FY23, and private capital projects ordering in 9MFY24 increased 33% YoY. Based upon this data, it is possible that some green shoots are already visible.

Our view:

India is currently enjoying the confluence of the macro and micro tailwinds with ~7% GDP growth, moderating inflation prints, range-bound crude prices, easing 10-year G-sec yield, stable currency, and resilient corporate earnings. Nifty is trading at a 12-month forward P/E ratio of ~20x, which is at a marginal premium to its long-term average. However, the NSE Midcap 100 index is trading at ~33% premium to Nifty.

Earnings growth trajectory, capex, policy initiatives like PLI, etc., Lok Sabha election outcome, and the timing and quantum of interest rate easing globally, will be monitorables for sustained valuations and market growth. This is even as India has outperformed the MSCI index: Over the last 12 months, the MSCI India Index (+36%) has outperformed the MSCI EM Index (+6%). Over the last 10 years, the MSCI India Index has notably outperformed the MSCI EM index by 214%.

We continue to believe that the investment environment going forward would be a “stock picker's market” and would separate the men from the boys. There could be instances where companies operating in the same sector may end up reporting diverse set of financial results. Our approach in such an environment would be the same as we have been following over the last few quarters. It would revolve around the thesis to identify companies basis the “bottom up” approach.

Our Risk Management Framework & our Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.

How are we positioned in our funds?

With macro situation being very dynamic and volatility increasing across asset classes, we continue with our strategy of running well-diversified portfolios. We are more focused on stock selection process within the sector rather than trying to take large overweight / underweight position among sectors. We would also refrain from taking aggressive cash calls. While the focus continues to be on stock selection on a bottom-up basis anchored on our “Investment Framework”, we would gradually tilt the portfolios towards large cap scrips compared to their midcap/small cap counter parts.

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility witnessed in the month of YTD CY24 to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain marginally above long-term averages. On the back of stable commodity prices especially crude oil and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy in CY24.

Investors wanting to invest in lumpsum should invest in ITI Balanced Advantage Fund, Value Fund and Long Term Equity Fund. Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs. While the current rally shows little signs of slowing down, retail investors must continue investing in well-managed funds via SIPs.