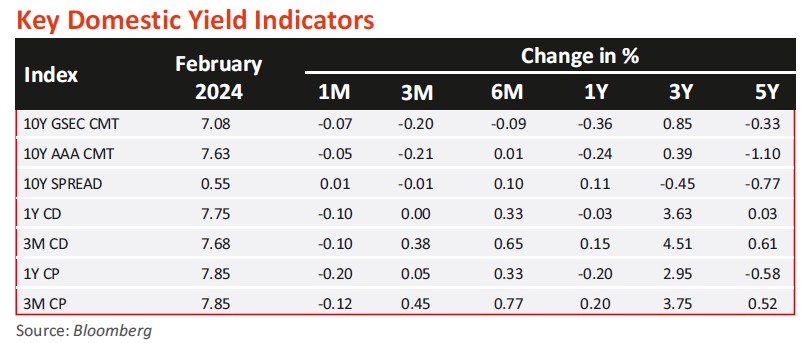

Debt Market Update

- India's third-quarter gross domestic product (GDP) grew at stronger-than-expected 8.4% as compared to the previous year. However, economists caution that this figure may be overstating actual economic growth. The 6.5% in GVA is a more mature measure and indicator of economic growth as it excludes indirect taxes and includes government subsidies. The large gap between GDP and GVA, declining agricultural activity, and a two-paced economic growth with investment outpacing consumption are matters of some concern.

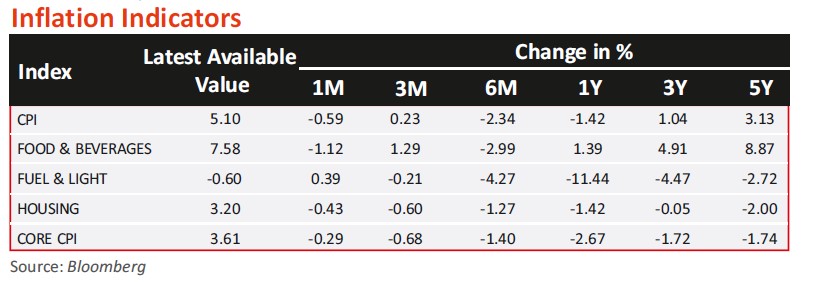

- Headline retail inflation (CPI) in January 2024 cooled to 5.10% (5.69% in December 2023), a 3-month low, on account of easing food prices. In a sign that the central bank’s monetary policy measures have been successful, core inflation has softened to 3.6% (3.9% in December 2023).

- December 2023 witnessed a surge in wholesale inflation (WPI) reaching a nine-month peak of 0.73%. For 2023-24 however, average WPI inflation remains in the deflationary zone at -1.1%. In December 2023, the price indices for all three major groups of the WPI were lower than the previous month viz. primary articles price index -2.1% MoM, fuel, and power price index -0.71% MoM, manufactured products price index -0.21% MoM. Consequently, the all-commodity index of the WPI fell 0.85% MoM, while the food index was 1.75% lower from November 2023.

- The growth in eight core sectors was 3.6% in January 2024, which marks the lowest growth in 15 months for the key infrastructure industries, including coal, crude oil, steel, cement, electricity, fertilizers, refinery products, and natural gas. In December 2023, core sector growth was initially reported at 3.8% before it was revised upward to 4.9%. In contrast, the output of the eight core sectors had seen significant growth of 9.7% in January 2023. Over April 2023 to January 2024, YoY output growth for the eight core industries was 7.7%, a slight decrease from the 8.3% recorded in the corresponding period last year.

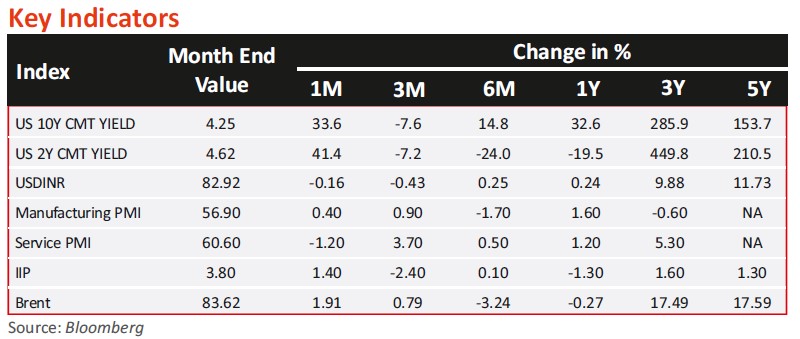

- India's industrial output (IIP) posted 3.8% growth marking an increase from the November 2023 figure of 2.4%. Comparatively, in December 2022, the industrial output had grown 5.1%. Over April-December 2023, the overall industrial growth scaled 6.1%, surpassing the 5.5% recorded in the same period in 2022. It is notable that industrial growth in December 2023 displayed resilience despite the core sector growth, a leading indicator, declining to a 14-month low of 3.8% from the previous month's 7.8%.

- GST collection in February 2024 touched Rs 1.68 lakh crore (Rs 1.72 lakh crore in January 2024), posting 12.5% YoY growth over the previous year.

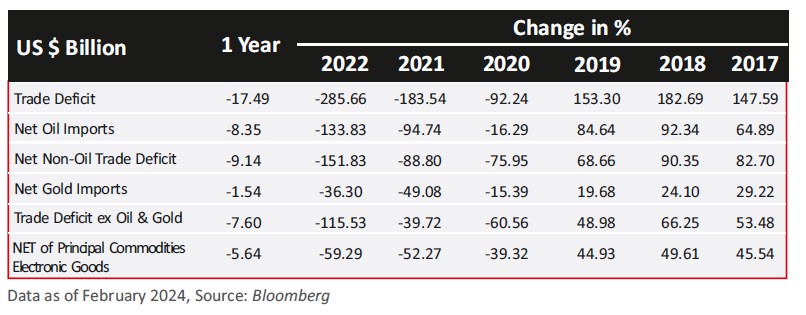

- India's merchandise trade deficit decreased to USD17.49bn in January 2024, the lowest in nine months, despite challenges posed by the Red Sea crisis and ongoing attacks on commercial vessels in the Suez Canal. Exports edged higher by 3.1% YoY to USD36.92bn. This improvement follows a December 2023 deficit of USD19.80bn, and the current trade gap is the smallest since April 2023. This underscores India's resilience in the face of global economic challenges, including the Red Sea crisis, recessions in advanced nations, and declining commodity prices.

- India’s fiscal deficit in 10MFY24 stood at ~64% of FY24RE. Gross tax revenue in 10MFY24 was ~79% of FY2024RE (14.5% higher) and net tax revenue was ~81% of FY2024RE (11.3% higher than 10MFY23). Total expenditure in 10MFY24RE increased to ~75% of FY2024RE (5.9% higher than 10MFY23), while capex at 76% of FY2024RE (27% higher).

Past performance may or may not be sustained in future and is not a guarantee of any future returns, and should not be used as a basis of comparison with other investments. Index performance does not signify scheme