Debt Market Update

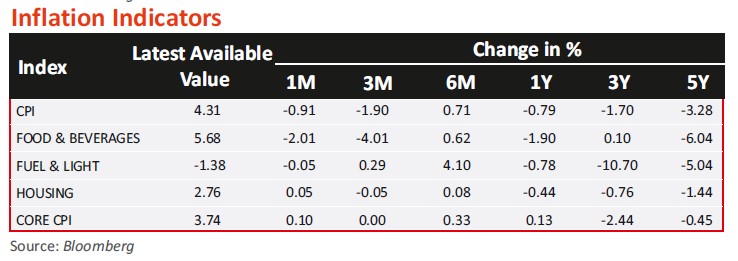

- India's CPI inflation fell to a five-month low of 4.31% in January 2025 as prices of vegetables and pulses eased, bringing respite to household budgets. The easing of inflation reflects a steadily declining trend after reaching a 14-month high of 6.21% in October 2024. CPI inflation had fallen to 5.48% in November 2024 and 5.22% in December 2024. Food inflation, at 6.02% in January 2025, is the lowest since August 2024. Support from fiscal and monetary policy is to narrow the negative output gap; unlikely to increase demand side inflation materially in FY26 and beyond. Tax cuts of INR 1trn, higher momentum of capital expenditure in FY26, and an effective monetary policy easing of about 75bps should be enough, in our view, to support a non-inflationary real GDP growth in of 6.5-7.0%.

- India's GDP growth for the third quarter of FY25 stood at 6.2%, marking a slight increase from the revised 5.6% in the previous quarter but a significant drop from the 8.6% growth recorded in the same quarter last year. This growth was largely driven by government consumption, which rose to 8.3% year-on-year (YoY), and private consumption, which grew at 6.9% YoY. The Gross Value Added (GVA) also grew at 6.2%, reflecting broad-based growth across sectors. Pickup in agriculture helps boost rural demand and private consumption growth outpaces GDP growth Real agriculture GVA clocked a splendid 5.6% y/y growth in Q3. Government incentives are driving higher private consumption, supported by rising rural demand. Fair progress of rabi sowing, tax breaks, and relaxations in risk weights for NBFC and MFI are in tandem expected to sustain consumption. While India's GDP growth in Q3 FY25 indicates a recovery from previous quarters, it remains below last year's levels. The government's upward revision of growth estimates for FY25 and historical years reflects optimism about the economy's potential.

- In the recent past, the Reserve Bank of India (RBI) has infused a significant amount of liquidity into the banking system through various measures. Different liquidity infusion steps taken by RBI are as follows:

- Open Market Operations (OMO) and Secondary Purchases: The RBI has purchased bonds worth approximately ₹1.39 trillion through open market and secondary purchase.

- Dollar/Rupee Swaps: A $5 billion dollar/rupee swap was conducted earlier, infusing around ₹44,000 crore into the system. A $10 billion three-year dollar/rupee swap is planned, which could infuse around ₹87,000 crore (approximately $10 billion) into the banking system.

- Variable Rate Repo (VRR) Auctions: 56-Day VRR Auction: The RBI conducted a 56-day VRR auction for ₹50,000 crore, which will mature around early April 2025. 49-Day VRR Auction: A 49-day VRR auction for ₹75,000 crore was conducted, also maturing around early April 2025. Daily VRR Auctions: The RBI has been conducting daily VRR auctions since January 2025, with reversals occurring the next working day, to address liquidity needs

- Total Liquidity Infusion: In the last five weeks, the RBI has infused more than ₹3.6 trillion of durable liquidity into the banking system through a combination of these measures. Despite these efforts, the banking system still faces a liquidity deficit, necessitating further infusions to ensure effective policy transmission

Source: RBI, Bloomberg, CCIL, MOSPI

*BE - Budget Estimates

Past performance may or may not be sustained in future and is not a guarantee of any future returns, and should not be used as a basis of comparison with other investments. Index performance does not signify scheme performance Investors should consult their financial advisers if in doubt about whether the product is suitable for them.