Dear Partners

Now that we are midway through FY23, we can take a glance at what has happened since March 2020, and come to an inference, especially with the benefit of hindsight, that despite lockdowns, commodity price spikes, inflation, policy rate hikes, adverse currency movements and the Ukraine war-led elevated risk environment, a steadfastly positive India macro outlook was the best position to hold onto.

Two of the structural positives for Indian corporates like the balance sheet strength at every level – government, corporates and households and economic policy stability after a period of disruptive reforms viz. demonetisation, GST, RERA, the bankruptcy law helped maintain this positive outlook.

Another key cushion was excess savings led by the ~US$ 200bn accretion to the forex reserves over Sep' 2019 to Feb' 2022 (Sources: RBI). This led to surplus liquidity of Rs 8tn built over this period, which in turn gave RBI enough firepower to protect the Indian Rupee by selling US$ and buying the Rupee this year. In spite of higher CAD/ FII selling, domestic liquidity in the banking system had a surplus of Rs 1.25tn due to which bond yields/ deposit rates did not surge. Resultantly, demand was not impacted, credit growth picking up drove demand and GST/ other tax collections remaining buoyant. This also gave the government strength to absorb higher fertiliser, oil and food prices and kept our inflation pressures on a leash, lowering the need for RBI to turn hawkish.

Now, as major global economies come under the threat of inflation and possible recession, leading to sustained tight monetary policy by Central banks worldwide, a legitimate concern of India also getting exposed to the next external shock increases too. While we should be aware of these intricacies and possible headwinds especially in the sectors with greater export or global connections, we need not react to this and watch if the war chest above gets rebuilt.

Hence, as external sector headwinds persist, some of the pressures have also been easing simultaneously:

- The RBI's monetary policy is in sync with global policy stance

- Commodity prices have fallen from their recent peaks

- Lower commodity prices would also lead to imports moderating and BOP deficit coming under control and improve forex reserves

- There is stability in capital inflows

- Domestic demand environment remains optimistic in the run-up to the festive season.

As mentioned by us earlier and what we feel is worth re-iterating are the structural positives for the Indian economy:

- India's corporate sector is in good shape. Aggregate profits of NSE 500 companies are set to double from Rs 5.20 lac crores in FY19 to over Rs 10.6 lac crores in the current year i.e. FY23. Leverage levels of corporate sector are low.

- India's banking sector is in good health, banks are well capitalised, historical NPAs are provided for. Despite Covid-19 led disruptions, asset quality has held up well.

- India's market share in global merchandise exports, which has been stagnant between CY10 to CY20, increased in CY21 led by global trends such as China plus one strategies and Governments policies such as PLI (Production-Linked Incentives). These are likely to lead to better export performance to fund our energy import deficit. IT exports and remittance remain strong.

- With both corporate and banking sector in good shape, we feel India is at the cusp of start of a domestic economic recovery cycle, which can lead to multi-year growth.

- Despite high energy prices and some slowdown in developed market economies and the Chinese economy, India's economic growth remains strong as reflected in various indicators such as Purchasing Managers Index numbers, electricity consumption, GST collections, property registrations etc.

- Our fiscal situation remains in control, with tax collections remaining strong.

Fiscal deficit, though higher than pre-Covid 19 levels is oriented towards higher capital expenditure. - External debt levels remain low and forex reserves are adequate to meet the projected CAD and external debt payments.

- Even with Crude oil at around USD 100-120/barrel, the Current account deficit for FY23 is likely to be around 3.5% of GDP, much lower than the 4.5% levels seen in FY12-13.

- Inflation differentials between India and developed world are much lower than the levels seen in FY13, hence the degree of liquidity tightening is likely to be much lower than seen in the previous periods of rate upcycle.

Even as India's 1QFY23 GDP grew at 13.5% YOY, it had a lower 1.3% CAGR over the past three years, indicating that there is further runway for the recovery to deepen into more segments of the economy and further corners of the country. The rural sector appears to be close to bottoming out. We may start seeing green shoots soon with a slightly above normal monsoon:

- Monsoon for June-Sept'22 has posted a surplus of 7%, although its distribution was uneven - deficiency was witnessed in UP, Bihar, Gangetic West Bengal. However, reservoir levels are at 88% of total capacity, which is much higher than long term average. While kharif output will be lower than last year, an overall late pick-up in monsoon could be beneficial for yields and the subsequent rabi crop.

- Although initial advance estimates for FY23 indicate a 4% decline in food grains and 1% decline in pulses for FY23, and a first decline in rice in 8 years, the stock of food grains is sufficient for the PDS requirement for this season.

- Crop and food prices with respect to cereals and pulses remain elevated, while oils and sugar are expected to soften. Vegetable prices continue to see impact from weather disturbances like delay in withdrawal of monsoon.

- State Governments are likely to start their capex programs with more intent now; they lagged in their capital expenditures due to liquidity constraints during the pandemic years. While usually, their combined capex is higher than that of the central government, in FY21 and FY22, as per data for 27 states, total capital expenditure by states fell below the Centre's levels. Now, of the Centre's interest-free loans of Rs. 1 trillion to states for capex, Rs. 34,000 crore has been allotted to 13 states and this amount is expected to rise. This, combined with a rebound in economic activities, is expected to mobilize enough revenue for states to push for higher capex, which will help provide a balanced economic recovery.

How are we positioned in our funds?

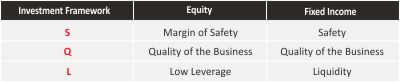

With macro situation being very dynamic and volatilities across asset classes increasing, we continue with our strategy of running well diversified portfolios. We are more focused on stock selections within the sector rather than trying to take large overweight / underweight positions among sectors. The focus continues to be on stock selection on a bottom-up basis anchored on our “SQL Investment Framework”

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. With markets having seen a good bounce back till August 2022, we saw some consolidation in September 2022. However, valuations remain slightly above long-term averages. We have observed in the past that whenever crude has corrected due to demand destruction in economic recessions, India's earnings growth and market performance have not remained immune. However, if crude prices correct due to increase in supplies, India will definitely benefit. Coupled with lower prices of other commodities too, and with operating leverage, earnings would rise for corporates, leading to a strong performance by the Indian economy.

Investors wanting to invest in lumpsum should invest in ITI Balanced Advantage Fund. More conservative investors can invest in ITI Conservative Hybrid Fund, which has the potential to give better returns than traditional savings products and with much lower volatility than that of equity or aggressive hybrid funds. Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs.

Our Investment Philosophy – SQL

Based on our combined investment learnings of more than 50 years, we have institutionalized very strong and unique investment Framework -SQL, which is core to our fund management framework and approach to our portfolios. We strongly believe that good quality (Q), low leverage companies (L) bought with a reasonable good margin of safety (S) makes the investment very attractive and rewarding for our investors.

Our Risk Management Framework

Our Risk Management Framework & our unique Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.